Watching Your Wallet: When Little Things Add Up

These past few months, we’ve found ourselves shopping online as a way to pass the time, spending $10 here and there.

What started out as “boredom browsing” often turned into a mini-shopping spree. Only, sometimes it wasn’t so “mini.”

It’s easy to forget how fast those small purchases add up, and before you know it, you have 8 different $10 packages at your doorstep.

Oops!

Using tags to track those impulse buys

To try to get a handle on it, we took a couple of weeks and tagged anything we bought that we didn’t really need as an Impulse Buy.

Dog food? Needed that. The little guy’s gotta eat!

Adorable dog collar? That was an Impulse Buy. (So cute though!)

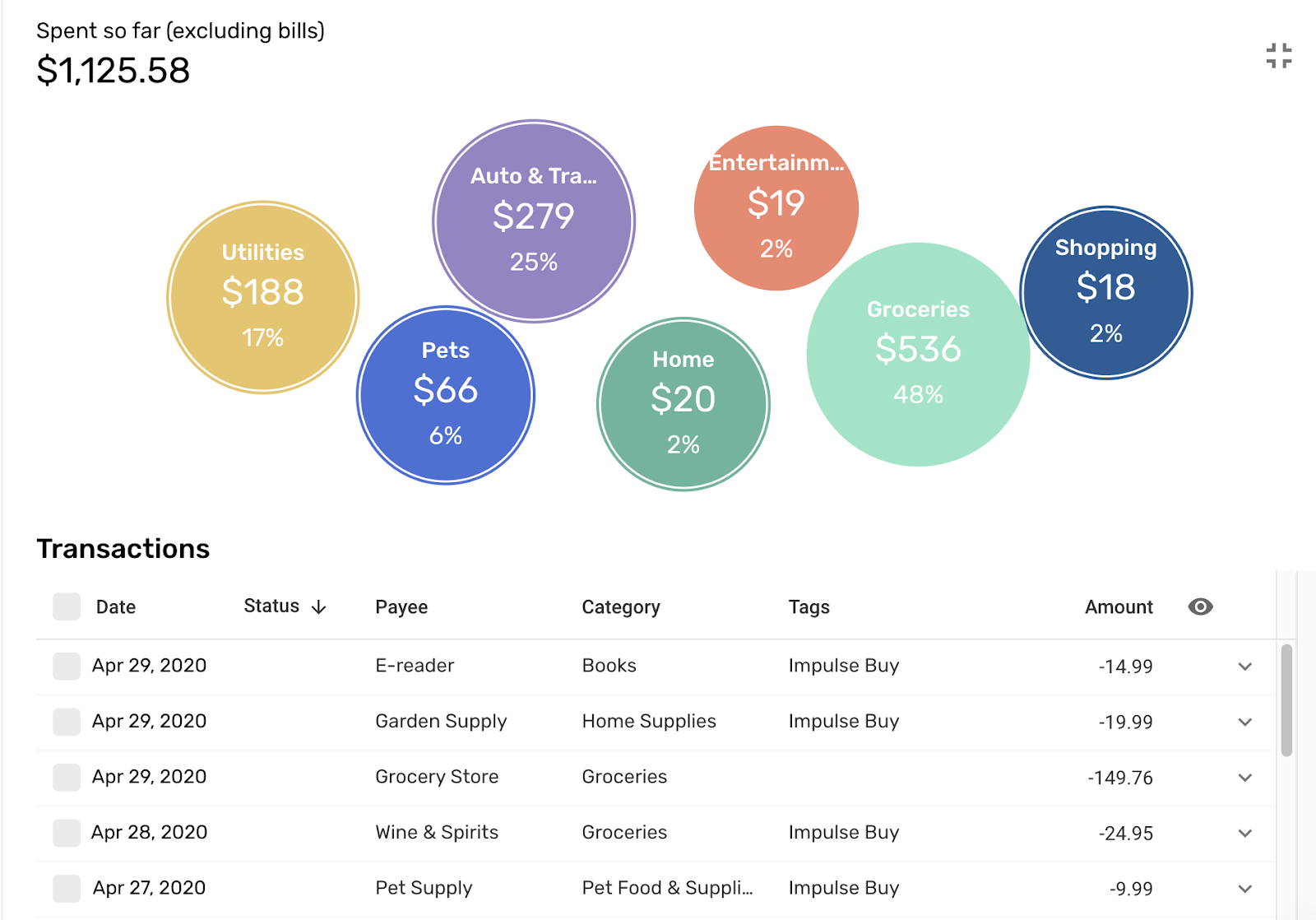

Tags are completely separate from categories. In the image above, you can see how categories track things like Groceries, Pets, and Entertainment. We used our Impulse Buy tag to track whether or not we needed each purchase, no matter what category it was in.

Here are some more highlights from our Impulse Buy lists:

- Video games on sale for $5.99 each

- 10 stickers for just $1 each, plus shipping (ugh)

- Cute pens for the home office (about $20 for the set)

- Wine – 2 cheap bottles

- Starbucks bottled drinks – a dozen over 2 weeks

By the time we were done, those small purchases were adding up to a real dent in our wallets.

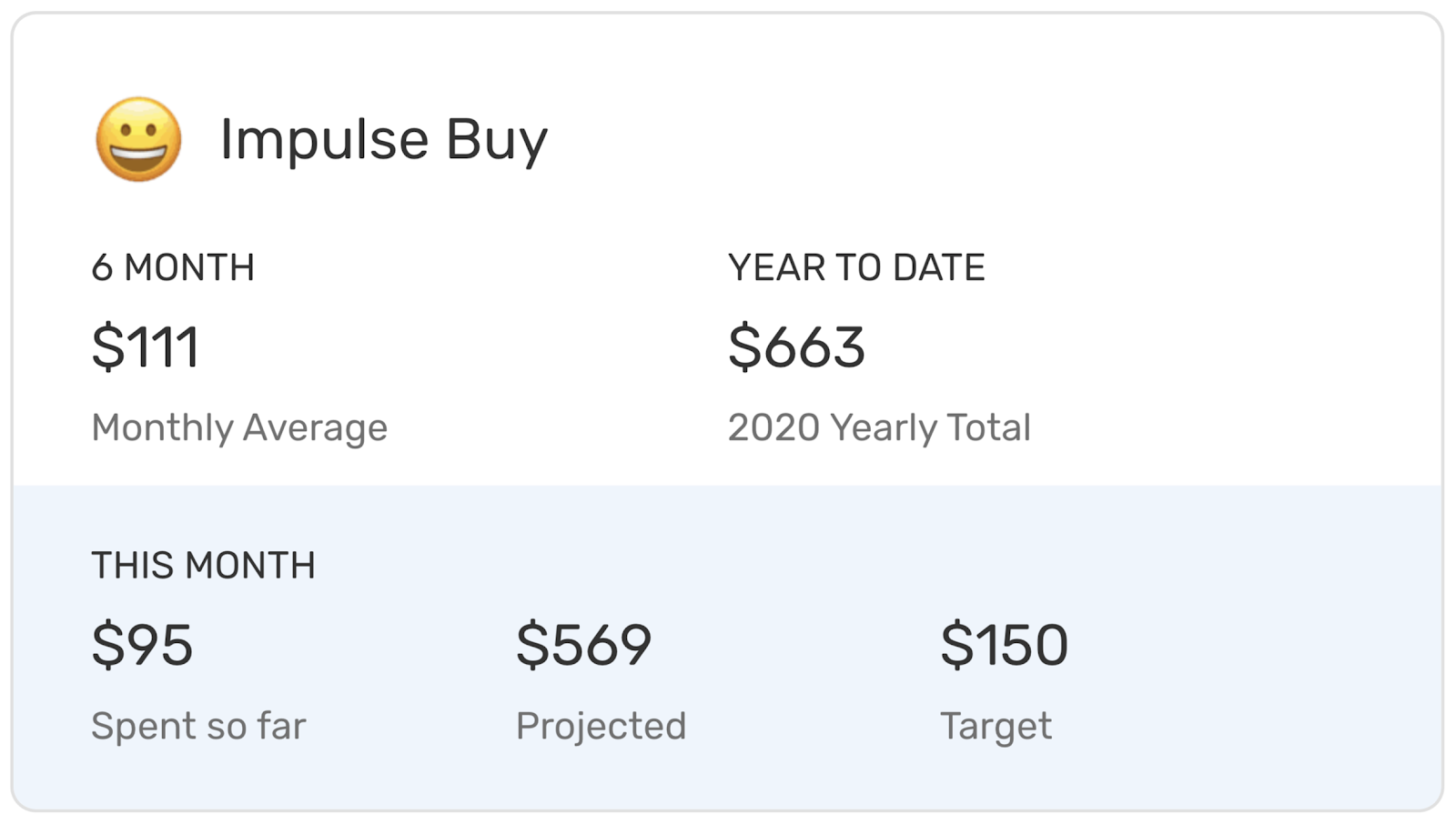

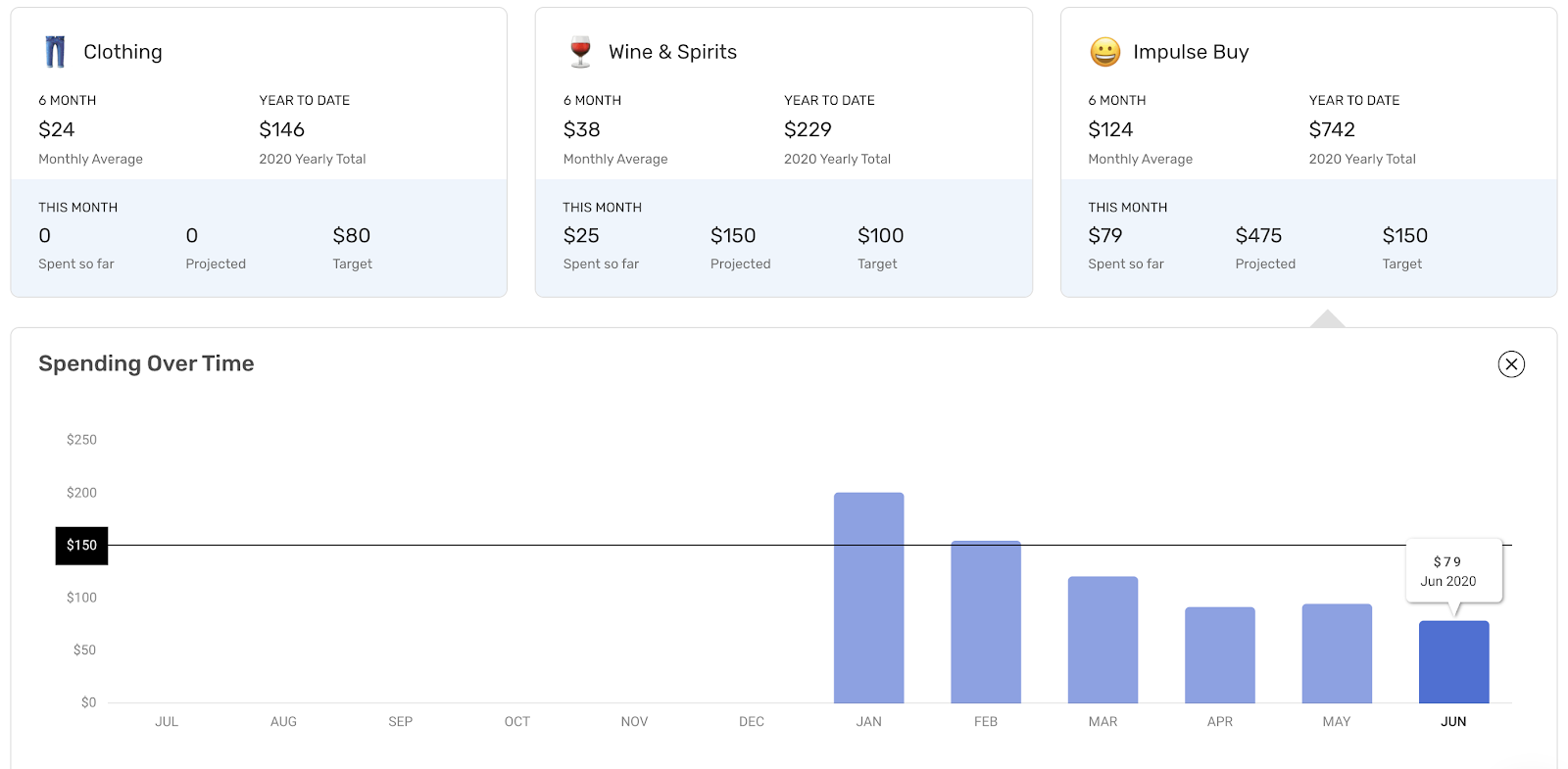

Using watchlists to track your tags

Since we created an Impulse Buy tag for our little experiment, we also created a watchlist for that tag to help us keep track of those splurge-shopping purchases as we made them.

We put a limit on it of $150—and blew right past that limit pretty quickly. We blame the wine. (Buying it, not drinking it. Take it from us, never shop online while tipsy. Just saying.)

Tracking that Impulse Buy spending through our watchlist helped us cut back on all those little orders—the ones that gave us a shopping high in the moment but didn’t make us feel good in the long run.

We still spent time shopping, but our watchlist kept it from getting out of hand. It also helped us pay more attention to each purchase, asking ourselves whether it was really worth it.

Cutting back, not cutting off

The thing about budgeting is that it has to be a balance. If you tried to cut yourself off completely from every indulgence, that would be hard to maintain and would leave you unhappy.

So, hey, if you grin every time you look at that adorable dog collar, it was probably worth that $10. Budgeting is about choosing those items carefully so they don’t add up fast to $100 (or more), taking away cash you could have used to add to your savings or pay down your debt.

Using watchlists can help you develop better habits and be smarter about avoiding splurges by:

- Thinking about that Impulse Buy purchase before you buy it

- Spreading your shopping out and saving some of it for later

- Setting a monthly limit so you don’t start racking up debt

Now that we’re using watchlists, we’re staying on top of our spending, still buying the occasional dog collar, and putting the rest of our spare cash toward paying down our debt—making those $10 decisions add up in a good way.

For more tips on staying on top of your finances, check out simplifimoney.com or download the Simplifi by Quicken app.

Quicken has made the material on this blog available for informational purposes only. Use of this website constitutes agreement to our Terms of Use and Privacy Policy. Quicken does not offer advisory or brokerage services, does not recommend the purchase or sale of any particular securities or other investments, and does not offer tax advice. For any such advice, please consult a professional.

{kind=link}

{kind=link}

{kind=link}