Take control of retirement planning with Quicken (Windows)

Note: This article is about the Retirement Calculator in Quicken for Windows. There is also a free tool available to everyone on our site.

Deciding how to save for your retirement is an important part of financial planning, and Quicken is here to help. Whether you are just starting out and looking at many years of savings, or are getting closer to retirement age and need to get back on track, the Quicken Retirement Calculator helps you take control of your planning.

By exploring your potential Annual Retirement Income, you can review items such as your annual contribution, savings, potential interest rate, and inflation changes to help you see how that will impact your eventual income. The calculator can also help you approach your planning from the perspective of your Annual Contribution or your Current Savings.

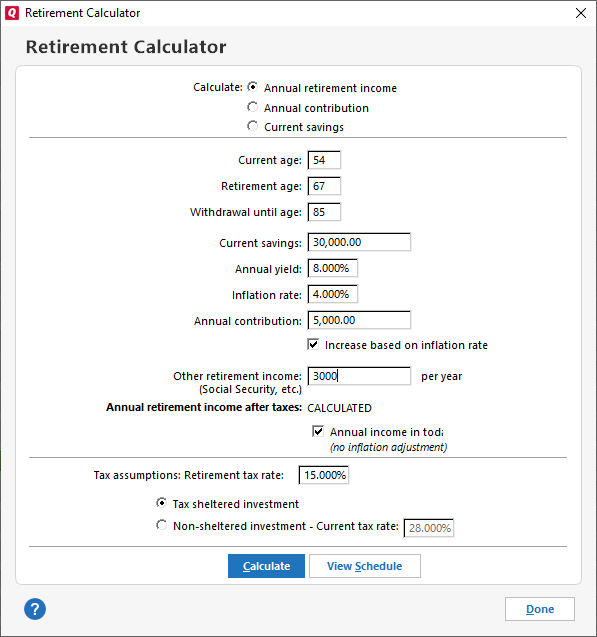

To use the Quicken Retirement Calculator, go to the Planning tab and select Planning tools → Retirement Calculator. You will then have the choice to base your planning on Annual retirement income, Annual contribution, or Current savings. In each case, the basic information you’ll provide will let you adjust your retirement age and other key factors related to your retirement.

The information you’ll need to provide or think about

To make the best use of the retirement calculator, you’ll want to have the key information for calculating your retirement income and the contributions necessary to get there.

To start with, you’ll want to think about ages. The retirement calculator will want your current age of course, but you’ll also need to think about the age when you want to retire, and how long you will need to have money coming in. Sixty-seven is the most common retirement age, but you may want to retire younger or be planning to wait longer. Withdrawal until age is a slightly more uncomfortable category. You are looking at the age for when you’ll no longer need money, which is a nice way of saying the age when you expect to die. It’s a sensitive topic, but one you should think about. Are you in great health and plan to stay that way? Do people in your family live a long time? Are there issues that make you think your time may be shorter? Try to be optimistic in your timeline.

You’ll then want to enter what your Current savings are. This includes any retirement account you have, such as an IRA or a 401(k). Anything that is dedicated to your retirement should be included in this number.

The next item, Annual yield, is what you expect your combined retirement accounts to earn. In some cases, you may have an exact percentage you can input, but usually, this is your best guess, and you should probably be conservative with this number. Six percent is a good starting point. It is a little less than what people expect to make in the stock market over the long term. If you have reason to believe your yield will be higher or lower, then go with your best estimate.

Deciding on an Inflation rate can also be a challenge and involves some guesswork. Most years over the past couple of decades, the inflation rate has been lower than three percent, but as we write this in late 2021, the inflation rate for this year may be higher than five percent. Try to pick a realistic number. Three percent is a good conservative estimate that will probably be higher than most years.

Your Annual contribution is a key number, which is why you can use this tool to calculate the right contribution for your situation. The contribution amount should include any automatic contributions you make, such as automatic withdrawals for a 401(k), as well as any matching contributions from your employer. You should also include any other amounts, such as if you have an investment account that is intended for your retirement.

For Other retirement income, you should also include your expected yearly income from Social Security or any pension plans you may have.

Finally, you should look at your Tax Assumption and whether or not you plan to use Tax sheltered investments. If you are using tax sheltered retirement accounts such as IRAs, annuities, and employer-sponsored 401(k)s and 403(b)s, use Tax sheltered investment. If your savings are outside of these areas, such as a general savings account or general stocks and bonds, then use Non-sheltered investment. In most cases, your retirement investments are probably tax sheltered. You’ll also want to estimate the retirement rate of your income once you retire. This will depend on what income bracket you expect to be in.

The results

Once you have entered all your information, click Calculate. Depending on whether you are calculating Annual retirement income, Annual contribution, or Current savings, the appropriate number will change.

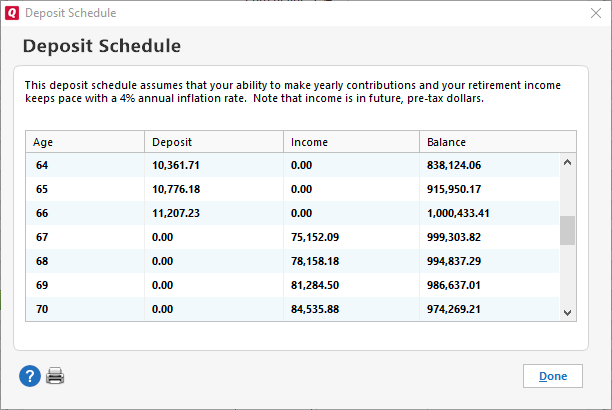

You can also click View Schedule to see a list of how much money you can plan to deposit or count as income each year of your retirement. This is a great way to see how the balance of your savings will be impacted year after year by your withdrawals.

The best use of the Retirement Calculator is to use it to start your planning, and then to check on the progress you are making. You should check in every six months or so, to make sure you are on track. If you want to delve deeper into planning for the future, you should also try the Lifetime Planner. The Lifetime Planner helps you plan for future purchases, assume different retirement ages for you and your spouse, and lets you explore more detailed future income or expense assumptions. To start using the Lifetime Planner go to the Planning tab and select the Lifetime Planner tab.

Quicken for Mac brings you three new budgeting features (Mac)

The team at Quicken for Mac is proud to introduce three new features for budgeting. These features will make it easier to track your categories by account, as well as to track your transfers and your detailed loan payments.

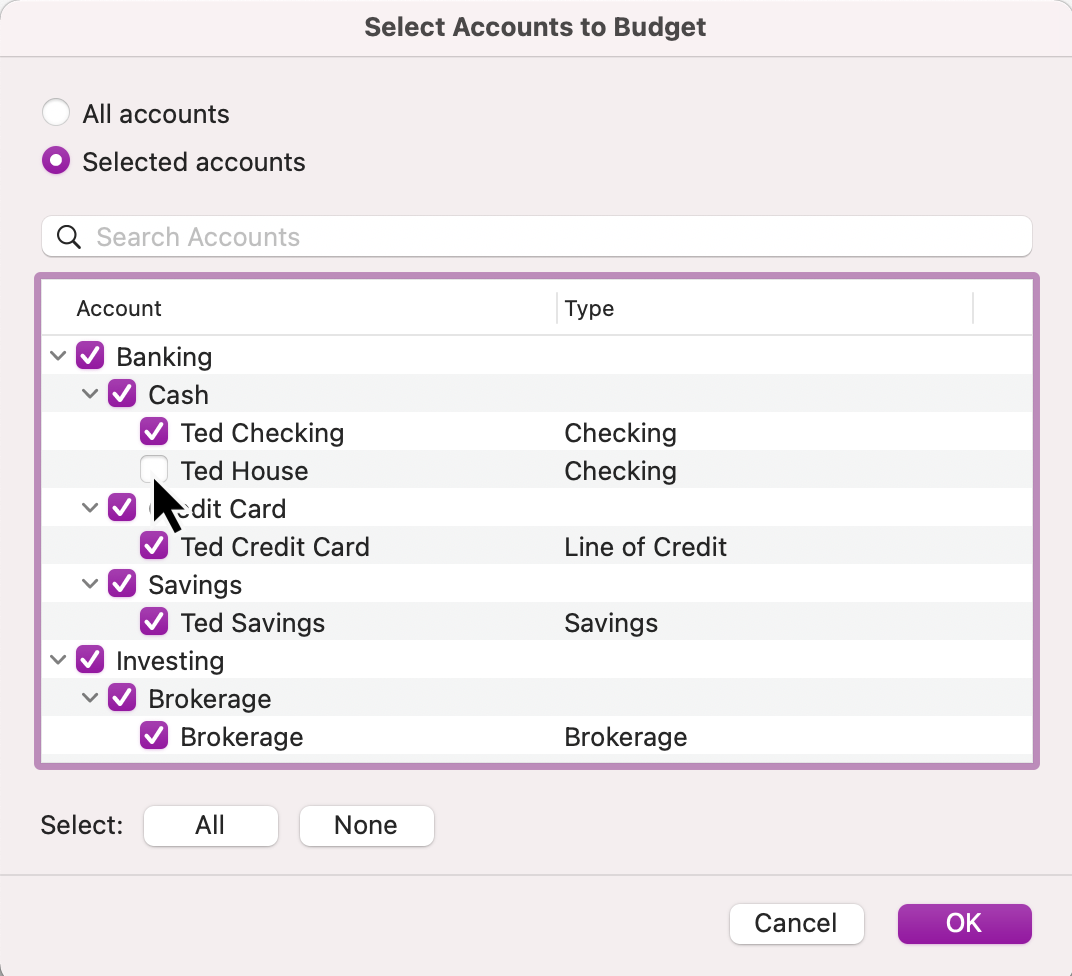

Track your budget by account

The ability to track your budget by account makes it much easier to exclude certain accounts from your budget. For example, if you have a shared account or an account set aside for a specific purpose, then you may want to exclude that account from your tracking.

To do this, go to Budgets menu → Edit Budget, then click Select Accounts at the bottom left of the screen. From there, choose Selected Accounts and deselect any accounts you want to exclude from your budget. This will allow you to continue to track the categories for those accounts without having them count toward your budget.

Track Transfers

Many people transfer money to or from other accounts as part of their income or spending. You may have an account designated for a child, a project, or another purpose such as a shared account. Now you can track these transfers as part of your budget.

To do this, go to the Budget tab and select Edit Budget, then click the Select Categories button at the bottom left of the screen. You will see two sections related to transfers, Transfer In and Transfer Out. Under those items are the specific accounts you can track transfers for. Just select the appropriate transfer and click OK to add it to your budget. You can then edit the budget amount on the Budget tab.

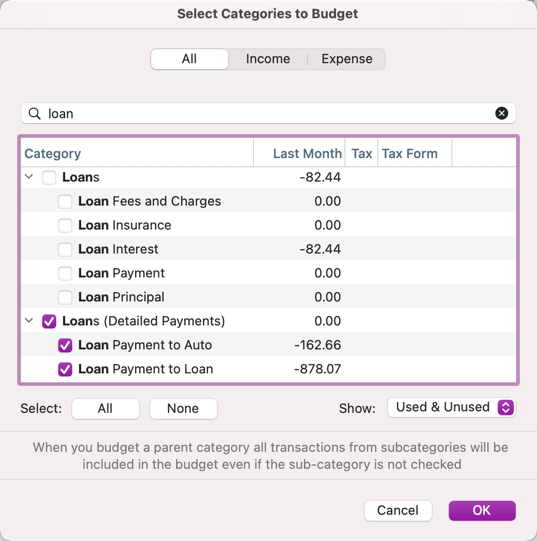

Use Detailed Loan Payments to streamline your budget

You could always track individual categories such as loan interest, loan principal, and loan payment, and now track your detailed loan payments as a category in your budget. For budget purposes, you may prefer to track the entire loan or mortgage payment, rather than the individual parts.

The new budget category Loans (Detailed Payment) displays all of the detailed payments that you have created in Quicken. This category is specifically for budget tracking, and is not a category you select for an individual transaction. Quicken calculates your detailed loan payment totals so that you can track them under Loans (Detailed Payment).

Quicken has made the material on this blog available for informational purposes only. Use of this website constitutes agreement to our Terms of Use and Privacy Policy. Quicken does not offer advisory or brokerage services, does not recommend the purchase or sale of any particular securities or other investments, and does not offer tax advice. For any such advice, please consult a professional.

Share article:

Post 250 of 826

About the Author

John Hewitt

John Hewitt is a Content Strategist for Quicken. He has many years of experience writing about personal finance and payment processing. In his spare time, he writes stories and poetry.

{kind=link}

{kind=link}

{kind=link}

{kind=link}